Loans can be lifesavers when you need funds for education, homeownership, or emergencies. However, failing to repay loans on time can lead to default, which brings financial and legal troubles. The good news? Loan defaults are avoidable with smart financial planning. Let’s explore the best strategies to stay on top of your loans and keep your finances healthy.

The Consequences of Loan Defaults

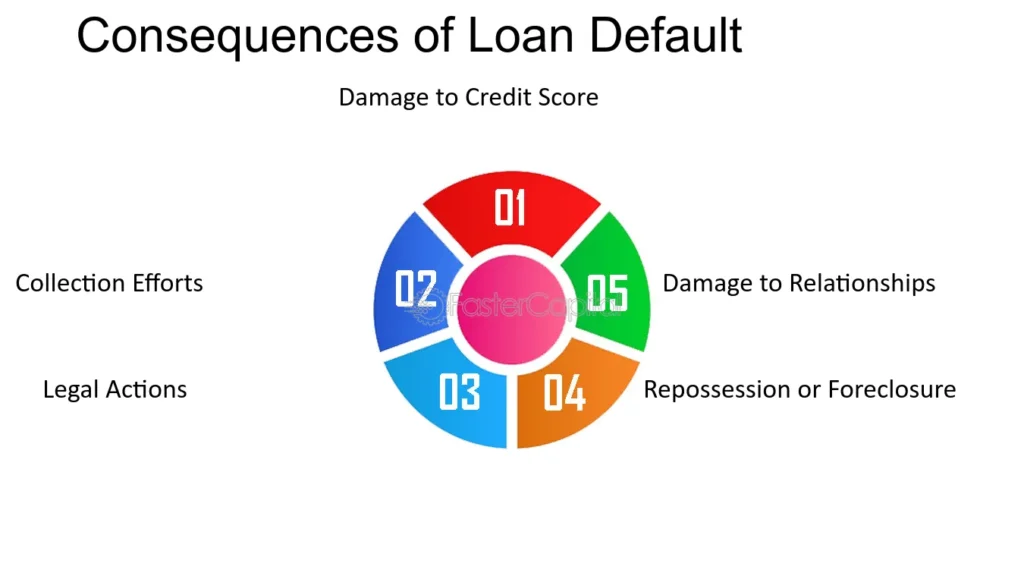

Loan defaults don’t just mean you owe money; they have serious repercussions that can impact your future financial stability.

Credit Score Damage

Your credit score takes a huge hit when you default on a loan. A low credit score makes it harder to get future loans, rent apartments, or even secure some jobs.

Legal Consequences

Lenders can take legal action against you, leading to wage garnishments, lawsuits, or even bankruptcy in extreme cases.

Asset Seizure

If you default on a secured loan (like a mortgage or car loan), the lender can seize your assets, such as your home or vehicle, to recover their losses.

Emotional Stress

Financial strain from a loan default can cause immense stress, anxiety, and even depression. Avoiding default ensures peace of mind.

Practical Tips to Avoid Loan Defaults

Budgeting and Financial Planning

A well-structured budget ensures you allocate enough funds for loan payments. Track your income and expenses to avoid financial pitfalls.

Understanding Loan Terms

Before signing any loan agreement, read the terms carefully. Know your interest rates, repayment period, and penalties for late payments.

Setting Up Automatic Payments

Automating loan payments prevents missed due dates and late fees. Most banks and lenders offer this feature to make payments hassle-free.

Effective Debt Management Strategies

Debt Consolidation

Consolidating multiple loans into one simplifies repayment and may reduce interest rates, making it easier to manage debts.

Refinancing Loans

Refinancing can lower monthly payments or interest rates, giving you more financial flexibility.

Prioritizing High-Interest Debt

Pay off high-interest loans first to reduce the total amount paid over time.

Building an Emergency Fund

Importance of Savings

Having a financial cushion helps cover unexpected expenses, reducing the risk of defaulting on loans.

Steps to Build an Emergency Fund

Start small by saving a portion of your income each month until you have at least three to six months’ worth of expenses saved.

Communicating with Lenders

Seeking Loan Modifications

If you’re struggling, ask your lender about modifying your loan terms to make payments more manageable.

Negotiating Payment Plans

Many lenders offer hardship programs or flexible payment plans if you communicate your financial struggles early.

Exploring Government Assistance Programs

Hardship Assistance

Some governments offer hardship assistance programs for those struggling to meet loan obligations.

Loan Forgiveness Programs

Programs such as student loan forgiveness can help reduce or eliminate debt under specific conditions.

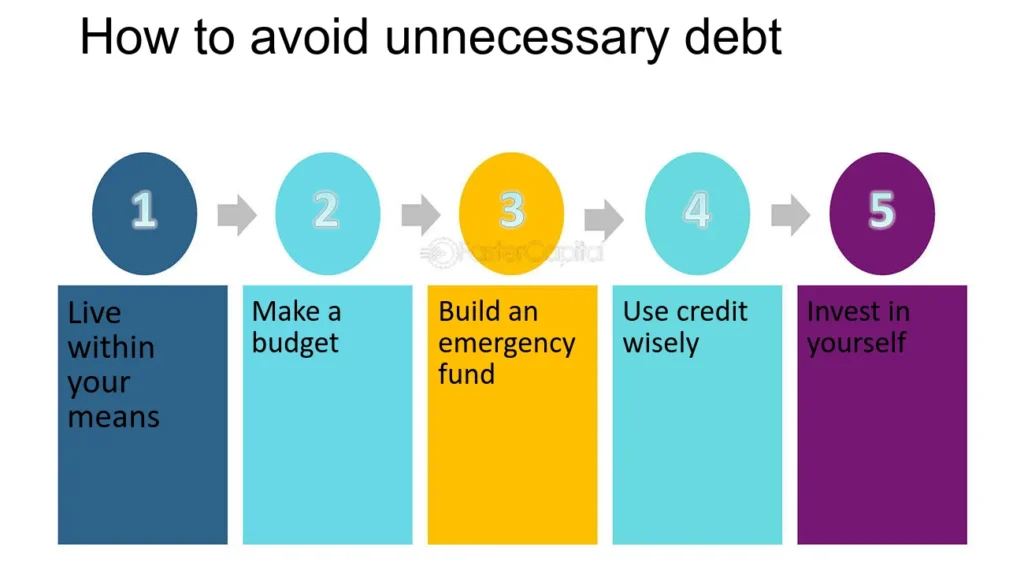

Avoiding Unnecessary Debt

Living Within Your Means

Avoid excessive borrowing by ensuring you only take loans you can realistically afford to repay.

Responsible Credit Card Usage

Credit cards can be helpful, but overusing them can lead to debt traps. Stick to spending within your means.

What to Do If You’re at Risk of Default

Recognizing the Warning Signs

Are you constantly late on payments or struggling with your finances? These are red flags that you might be heading toward default.

Seeking Financial Counseling

Nonprofit credit counseling services can provide guidance on managing debt and creating a repayment plan.

Conclusion

Avoiding loan defaults requires discipline, smart financial planning, and proactive communication with lenders. By budgeting wisely, building an emergency fund, and seeking assistance when needed, you can stay ahead of your loan payments and protect your financial future.

FAQs

1. How can I rebuild my credit after defaulting on a loan?

Start by making consistent, on-time payments, reducing credit utilization, and using secured credit cards to gradually improve your score.

2. Can a lender sue me for defaulting on a loan?

Yes, lenders can take legal action, which may lead to wage garnishment or asset seizure.

3. What should I do if I can’t afford my loan payments anymore?

Contact your lender immediately to discuss restructuring options, loan deferment, or payment extensions.

4. Is debt consolidation a good option to avoid default?

Yes, consolidating loans can make repayment easier by combining multiple debts into one with a lower interest rate.

5. How much should I save in an emergency fund to avoid loan defaults?

Aim for at least three to six months’ worth of expenses to cover unexpected financial hardships.