What is Loan Consolidation?

Loan consolidation is the process of combining multiple debts into a single loan with one monthly payment. This can make managing your debt easier and potentially lower your overall interest rate.

Why Consider Loan Consolidation?

If you’re struggling to keep up with multiple loan payments, consolidation might be a lifesaver. It can simplify your finances, reduce stress, and even improve your credit score over time.

Understanding Loan Consolidation

How Does Loan Consolidation Work?

When you consolidate your loans, a lender pays off your existing debts and gives you a new loan with a single monthly payment. The goal is to make repayment easier and more manageable.

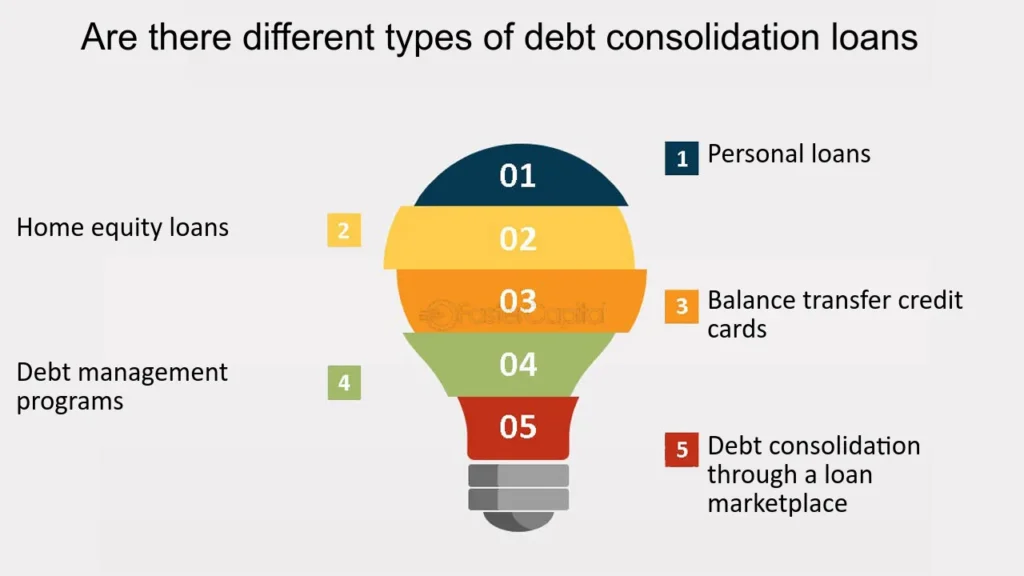

Different Types of Loan Consolidation

- Secured Loan Consolidation: Requires collateral, such as a house or car.

- Unsecured Loan Consolidation: Doesn’t require collateral but may have higher interest rates.

Benefits of Loan Consolidation

Lower Interest Rates

Consolidating high-interest debts, like credit card balances, can help you secure a lower interest rate.

Simplified Repayments

Instead of juggling multiple due dates, you’ll have just one payment to worry about.

Improved Credit Score

Consistently making on-time payments on your consolidated loan can boost your credit score.

Fixed Payment Schedule

You’ll know exactly how much you owe each month, making it easier to budget.

Types of Loans Eligible for Consolidation

- Student Loans

- Credit Card Debt

- Personal Loans

- Auto Loans

- Medical Bills

Loan Consolidation Methods

Balance Transfer Credit Cards

These allow you to transfer high-interest debt onto a card with a lower interest rate.

Personal Loans

A personal loan can be used to pay off multiple debts, leaving you with a single repayment.

Home Equity Loans

If you own a home, you can use your home equity to consolidate debt.

Debt Management Plans

Working with a credit counseling agency can help you negotiate better repayment terms.

Steps to Consolidate Your Loans

- Assess Your Debt – Know how much you owe and to whom.

- Research Lenders – Look for reputable lenders with competitive interest rates.

- Check Eligibility – Ensure you qualify for a consolidation loan.

- Compare Interest Rates – Choose the best option available.

- Apply for Loan Consolidation – Submit your application and start repaying.

Common Mistakes to Avoid

- Ignoring hidden fees.

- Not comparing lenders before choosing a loan.

- Choosing a longer repayment term without considering the extra interest.

- Impact of Loan Consolidation on Credit Score

How Your Credit Score Can Improve

- Reduces credit utilization ratio.

- Helps establish a history of on-time payments.

- Short-term vs. Long-term Effects

Initially, your score may drop slightly due to a hard credit inquiry, but over time, responsible repayment can significantly improve it.

Government Programs for Loan Consolidation

- Federal Loan Consolidation for Students

- State-Level Debt Relief Programs

Tips for Managing Consolidated Loans

- Stick to a budget.

- Avoid taking on new debt.

- Set up automatic payments to avoid missed deadlines.

Conclusion

Consolidating your loans can be a smart financial move if done correctly. It simplifies your finances, potentially lowers interest rates, and improves your credit score. However, it’s crucial to choose the right consolidation method and avoid common pitfalls.

FAQs

1. What is the best loan consolidation method?

The best method depends on your financial situation. Personal loans and balance transfer cards are popular options.

2. Does consolidating loans hurt my credit?

Initially, it may cause a slight dip in your score, but long-term, it can improve your credit if managed properly.

3. How long does loan consolidation take?

The process can take anywhere from a few days to a few weeks, depending on the lender and type of consolidation.

4. Can I consolidate all my debts into one loan?

It depends on the lender and your creditworthiness. Some lenders have restrictions on the types of debt they accept.

5. What happens if I miss a payment on my consolidated loan?

Missing payments can lead to late fees, increased interest rates, and a negative impact on your credit score. Always set up automatic payments if possible.